Solutions

Growth Can Return While Profitability Lags

Learn why strong growth isn't translating into profits and discover strategic shifts for business resiliency in our upcoming webinar.

Are corporate profits plunging? Explore the latest analysis on US corporate profits, industry trends, and strategic advice to navigate economic cycles.

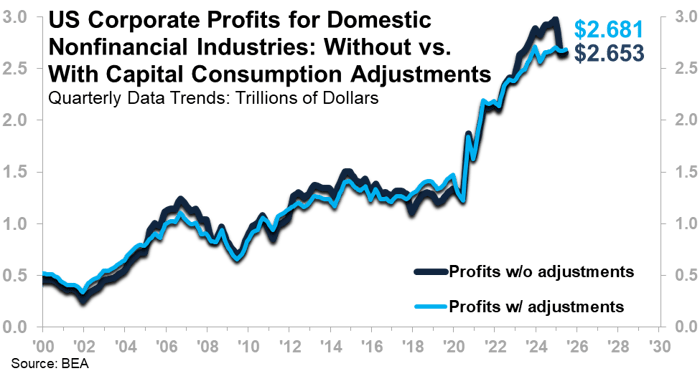

The latest data from the US Bureau of Economic Analysis (BEA) reports that US Corporate Profits for Domestic Nonfinancial Industries have declined to $2.65 trillion in the second quarter of 2025, a 10.8% drop from the December 2024 peak.

However, special tax provisions during certain periods of history can overstate or understate profits. For example, the One Big Beautiful Bill Act (OBBBA) passed earlier this year restored the use of bonus depreciation, a special tax provision that can allow firms to recognize lower profit levels than they would otherwise be able to. The results change significantly if we look at profits after the BEA applies a capital consumption adjustment to account for this issue. Adjusted Nonfinancial Profits came in at $2.68 trillion in the second quarter of 2025, only 1.1% below the late-2023 record high.

Nonetheless, a tick down in Corporate Profits is not unexpected; ITR Economics has been warning of the risk of “profitless prosperity” during the 2020s. This happens when top-line metrics rise thanks in no small part to inflation, but the bottom line suffers as elevated interest rates, elevated labor and material costs, and other pressures impede profitability. While such an environment may call for more careful decision-making, it is not cause for panic. Corporate profits, like the broader economy, move through cycles of accelerating growth, slowing growth, contraction, and recovery. The high-inflation, low-interest-rate, stimulus-driven environment that followed the pandemic likely means that some post-COVID correction is inevitable. Current indicators suggest movements in corporate profits are more of a yellow flag, or a slowdown worth watching, than a harbinger of systemic macroeconomic decline.

Industry-level profit trends vary widely, showing that sector positioning matters. Presented below are industry-level corporate profits; keep in mind that we are presenting these profits without capital adjustments, because that is the only industry profit data available from the source. Non-adjusted profits may understate or overstate stated profits during certain periods.

| Industry | % Change 2Q25 vs. 2Q24 | Phase |

| Financial | +13.2% | C – Slowing Growth |

| Chemical Products | +7.5% | B – Accelerating Growth |

| Retail Trade | +1.1% | B – Accelerating Growth |

| Information | -5.2% | D – Recession |

| Utilities | -20.6% | D – Recession |

| Wholesale Trade | -26.2% | D – Recession |

| Machinery | -29.3% | D – Recession |

A downturn in profits is not a signal for permanent decline. Even after the recent tick down, non-financial corporate profits adjusted for inflation, capital consumption, and inventories are 25.7% above the ten-year average. In addition, corporate profits for many of the sectors in the table above are also elevated relative to historical averages, despite the fact that some of them are in Phase D, Recession (we define Phase D as down year over year, with the pace of contraction intensifying). Based on this, we have the following advice for firms:

Today’s profit softness is a natural reset. Businesses that stay analytical and forward-focused will be best-positioned for the next growth phase. Ensure that you are taking advantage of a slight dip in interest rates to consider what capex projects make sense and which do not as far as combatting profitless prosperity: where the top line rises, but the bottom line remains under pressure. Investment in efficiencies or new markets with a short ROI is the medicine we prescribe for most businesses.

Learn why strong growth isn't translating into profits and discover strategic shifts for business resiliency in our upcoming webinar.

Discover why strong growth isn't translating into profits and learn strategic shifts for business resiliency in our upcoming webinar.

Just-released Corporate Profits data shows that Corporate Profits (with capital consumption adjustments) are rising after reaching a low in March...