Recent leading indicators suggest that nonresidential construction activity will be rebounding as we head into the second half of 2021 and beyond.

The initial macroeconomic carnage brought on by COVID-19 in early 2020 has lingered in nonresidential construction markets thus far into 2021. Due to nonresidential construction consisting of larger projects that require longer planning horizons and more capital than its residential counterpart, this is a lagging sector of the economy; it takes more time to fully absorb disturbances at the macroeconomic level. The data is indicating that this market is starting to turn the corner.

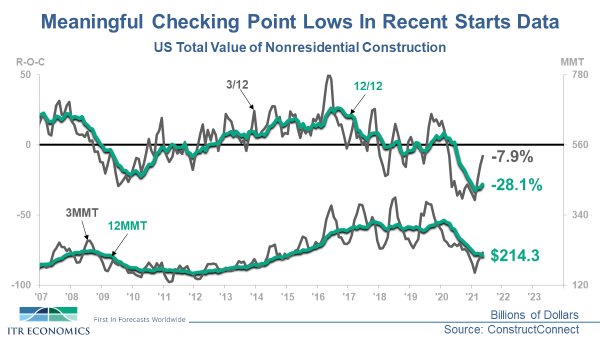

US Total Value of Nonresidential Construction Starts, published by ConstructConnect, has tentatively transitioned to recovery, a recovery trend that appears viable based on leading indicator support. On an annualized basis Starts are still down 28.1% from the year-ago level, but on a quarterly basis the bleeding is slowing. This is generally ‘on time’ with what we typically see as a one-year lag time between the US economy and nonresidential construction markets, though it can vary by individual sector. US Gross Domestic Product reached a cyclical low at the end of the second quarter of 2020 and immediately moved into recovery thereafter; add a year and that lands us in mid-2021, right on time.

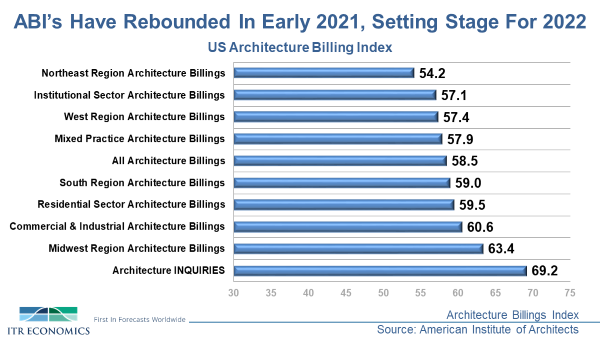

Industry specific leading indicators are encouraging as well, as a general canvas of the various Architecture Billings Index data from the American Institute of Architects paints a positive picture for the industry.

All of these raw monthly readings are above 50.0, a diffusion index designation that indicates improvement in Billings activity in the various sectors from the prior month. ITR takes the additional step of generating rates-of-change on these data points and correlating them to nonresidential construction markets. On a rate-of-change basis we see definitive upward momentum as well.

There are lingering risks and concerns in some markets, to be sure. Elevated vacancies in commercial office space is one example, as the dust from defining whatever will be ‘normal’ post-COVID continues to settle. However, the aggregation of these data points indicate increasing builder and project owner confidence and a rising tide for a sector that has lagged the recovery to this point. Expect more project and bid prospects to come in the quarters ahead. Prioritize better fit and higher profit opportunities as the leaner days in the market are fading behind us.

Connor Lokar

Economist