Abject pessimism will not help you effectively prepare for the upcoming downturn. Here are a couple more datapoints that support our expectation that next year’s recession will be relatively mild.

Supply Chain Tightness Is Easing

The Global Supply Chain Pressure Index, published by the Federal Reserve Bank of New York, came in with negative readings for February and March; negative readings in the Index indicate a below-average level of pressure – i.e., disruption – in the supply chain. Mid-2019 was the last time the Index indicated below-average pressure.

Keep in mind that the supply chain improvements will not be (and have not been) uniform across sectors or products. Our clients report that while overall conditions have generally improved, they will still often find themselves having to scramble to obtain that “golden screw” – the “one little thing” they need to complete their product. However, those that have built up a hearty cash reserve may gain the opportunity to buy their own golden screw factory when the 2024 downturn sets in.

Still-High Backlogs

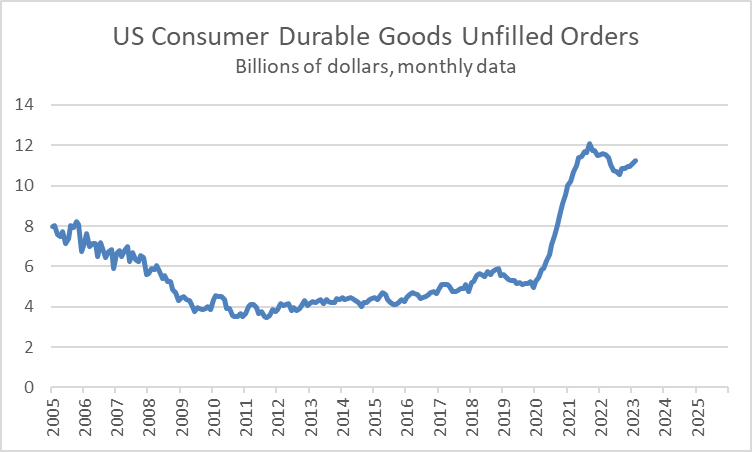

Our clients and audiences are reporting high backlogs, which is another factor behind our expectation that 2024’s macroeconomic downturn will be relatively mild. We expect that even as new orders decline, producers will have backlogs to keep them relatively active. These anecdotal inputs from our industrial sector contacts bear out in the downstream data; US Consumer Durable Goods Unfilled Orders are still high relative to pre-pandemic numbers.

Adjusted for inflation, the level of Unfilled Orders is also elevated, but the data slipped below year-earlier levels. Companies need to look at volume, or deflated data, in addition to simple nominal dollars when gauging the strength of their own backlog.

Furthermore, keep in mind that order cancellations tend to become a bigger problem during periods of slowing growth and recession.

At ITR Economics, we encourage optimism, but also caution. The above factors could prove less beneficial if the Federal Reserve remains hawkish, pushing up interest rates further to the point that business and consumer activity is dampened beyond our current expectations. Follow along with our Fed Watch series for our take on developments related to the Fed.