Industry Updates

Do Not Fear the Future

The April 2020 to April 2019 year-over-year comparison (1/12 rate-of-change) posted the steepest decline on record.

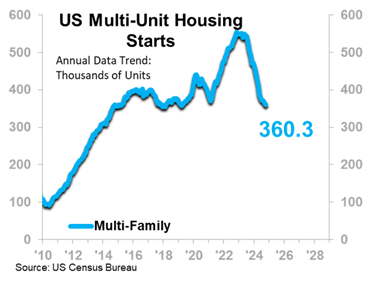

US Multi-Family Housing Starts is showing signs of recovery as the rate of decline slows. Find out what is in store for the segment in 2025!

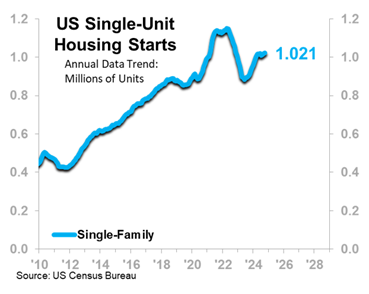

Previously, we discussed the US Single-Unit Housing Starts trend, a key bellwether for the overall US economy, and how it has recovered and stalled once again in the wake of the decline that occurred from mid-2022 to mid-2023.

Housing affordability has been an issue since the COVID-related boom that preceded the aforementioned steep decline.

A market that gets less attention is US Multi-Unit Housing Starts, partially because it accounts for a smaller overall portion of the overall housing construction market, and also because it is less reliable as a leading indicator to the US economy. Additionally, the multi-family market provides less of an advance warning due its lead time of about 3-4 months relative to Single-Unit Starts’ 9-month lead.

Still, the multi-family segment is a significant part of the housing market, and it is worth noting that the Multi-Unit Starts 12MMT has been on a decidedly downward trajectory since the Fed took a hawkish tack in 2022 and 2023, raising the target interest rate an average of 31 basis points per month for 17 months.

Despite this negativity, the multi-family market is on the cusp of a positive trend.

In Phase A, it can be difficult to believe that Phase B is coming.

In the day-to-day, as your view of the market and your revenue stemming from the market go down, and inquiries are fewer and farther between, it is easy to identify that the market is declining. It is harder to discern that the rate of decline is easing as a prelude to eventual recovery. Even when you calculate your rates-of-change and identify with mathematical certainty that the rate of decline is indeed easing, it is emotionally difficult to accept that the decline will slow, the data will reach a low, and rise will take hold thereafter.

But at ITR Economics, we have seen it happen time and again. If you have data for your company going back at least several years, we can likely show you where it happened for you in the past.

For Multi-Unit Housing Starts, it happened in 2010 and 2018.

With Phase A expected to give way to Phase B in in the second half of 2025, business leaders involved in the multi-family housing construction market need to prepare for the forthcoming rising trend.

For more about the multi-unit market or what to do at this juncture of the business cycle, contact us at ITR Economics.

The April 2020 to April 2019 year-over-year comparison (1/12 rate-of-change) posted the steepest decline on record.

Tune in to this Business Series Webinar as Senior Forecaster Connor Lokar reviews the inflationary trends of the 2020s and their impact on businesses.

To help nonresidential construction businesses strategize for the 2030s depression, these 4 pieces of advice will help you through the rest of the...