The Federal Reserve raised the federal funds target rate by 75 basis points on June 15. The stock market seemed to be pleased at the attempt to quell inflation. That didn’t last long, with the S&P 500 dropping 3.7% the very next day.

Recession fears are amped up; one point of view is that the Federal Reserve will push interest rates too high and create a recession as they try to stamp out inflation. We totally understand the fear, and the Fed’s track record is less than stellar. However, going down that line of thinking may be giving the Fed credit for power they do not have. Or, they have more wisdom than the marketplace is currently crediting to them. The charts below provide some hope and cause for optimism.

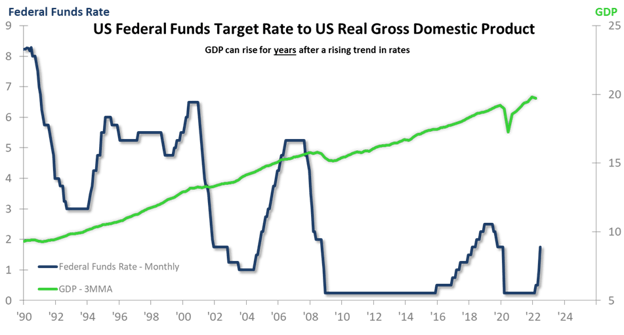

The first chart shows that the Fed can push (and has pushed) interest rates up for years before the economy, as measured by GDP (adjusted for inflation), stalls out and/or declines. As a side bar, it is interesting to note that the Fed has a tendency to stop raising interest rates before the actual recession begins, but that doesn’t mean they don’t push their quest too far.

Our primary takeaway from the historical record is that the emotional relationship between rising interest rates and a business cycle recession is understandable, but most people get the timing of the relationship wrong. In this instance, because consumer balance sheets are in a strong position (based on Federal Reserve data), a shorter-than-normal lead time to a recession is not probable.

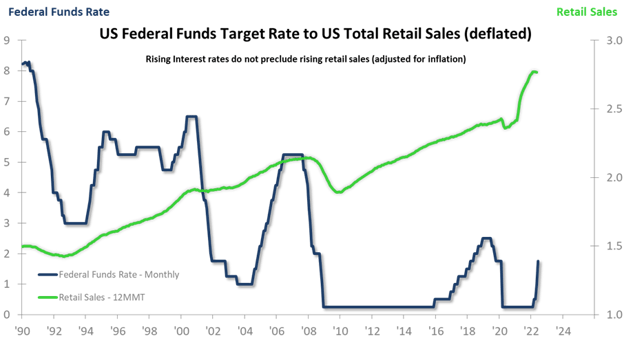

The next slide compares the federal funds rate trend to US Total Retail Sales (adjusted for inflation). We see that Retail Sales will rise for years after the Fed starts pushing rates higher. Steep ascents occurred in the past. They were not immediately ruinous.

A complicating factor for us at present is the abnormal rise prior to 2021 stemming from the extreme stimulus provided by Congress and the Fed in response to the pandemic. The Retail Sales 12MMT data trend has leveled off. The emotions immediately jump to tying that flatness to rising interest rates. The more probable reality is that the withdrawal of artificial stimulation has more to do with the new lack of rise in the Retail Sales 12MMT. A return to normalcy is going to be a process that involves slower Retail Sales growth than we saw in 2021.

ITR forecasted that this flat spot would occur. We think the Retail Sales 12MMT will be slightly down/slightly up into the fourth quarter of 2022 before a more positive trend develops for 2023. We do not think that we suddenly live in a world of instantaneous cause and effect when it comes to economics. There is no evidence beyond the emotional connection that our world has changed that much.

The above does not mean that all sectors of the US economy will continue to blissfully grow in the years immediately ahead. For instance, housing is more interest sensitive; it is also a leading indicator to GDP. We are reassessing our US Housing Starts outlook based on the latest hike and resulting trend probabilities. It is possible we may need to lower our current forecast for Housing Starts through 2024. Beyond mortgage rates, there are demographics, inventories, and investment buyers to consider.