Executive Strategy

'Has Your Outlook for 2023 Changed?'

One of the most frequent questions we are getting lately is “Has your outlook for 2023 changed?” The answer: yes and no.

ITR Economics has changed its forecast for GDP (in inflation-adjusted dollars). See what has changed and what remains the same in our blog.

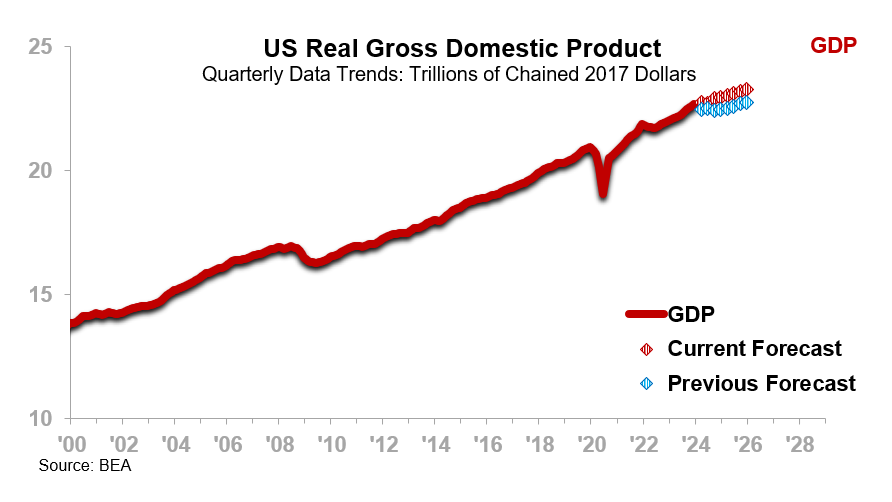

We have changed our forecast for GDP (in inflation-adjusted dollars). Before we get into the details, it is important to note that the change was not dramatic, and it does not change the Management Objectives™ that we discuss with our consulting clients and present in keynotes, blog posts, and TrendsTalk.

If you are a service business, you are less likely to experience downside economic pressures on your business in 2024 than we had previously expected. This means you may see less slowing in your company’s rate of growth in 2024 than we were previously anticipating. A recession in GDP, which most people equate with “the economy,” was not part of the previous outlook.

ITR Economics’ forecast for the industrial portion of the economy has not changed. Results through December have a 0.0% deviation from the forecast we put in place in mid-2023 (12MMA). We continue to forecast that Industrial Production will decline until late 2024, as indicated by a wide range of economic inputs. There is potential for the decline to extend into early 2025. Many, though by no means all, of the industry trends that comprise Industrial Production will move with the overarching Industrial Production trend. Industrial Production encompasses manufacturing, mining, and utilities. Many wholesalers, distributors, and others servicing the industrial segment of the economy are also likely to see a decline in revenue.

GDP performance in the second half of 2023 was stronger than we had anticipated. We underestimated the impact of the tremendous investment by the government in infrastructure and via the CHIPS and Science Act. Profit levels and cash balances in corporations held up very well despite the headwinds of slower growth in capital expenditures, high interest rates, and monetary policy. The January job numbers were also an important consideration, as they speak to more strength than previously anticipated in consumer spending, which is always a plus for the overall economy. Consumer health is looking good, which is an important driver to mild rise in GDP in 2024.

There are downside risks to the GDP forecast for 2024. Specifically:

The key to the change is understanding where your company fits into the economy. The service sector in general will experience a slowing in the rate of growth, but the key is knowing what is likely to happen in your particular industry. It is financially painful to plan on slower growth and then find out that it was time to push the accelerator to the floor. The industrial sector outlook has not changed, and EVP™ clients and others who follow our forecasts for the industrial sector should stay the course.

One of the most frequent questions we are getting lately is “Has your outlook for 2023 changed?” The answer: yes and no.

We can understand why folks wonder how the forecasting accuracy has fared owing to all the political commentary, tariffs, regulatory changes, etc.

This isn’t the first time the number of EU member countries has changed, but the UK's leaving was the most noticeable change in many years.