Do Not Fear the Future

The April 2020 to April 2019 year-over-year comparison (1/12 rate-of-change) posted the steepest decline on record.

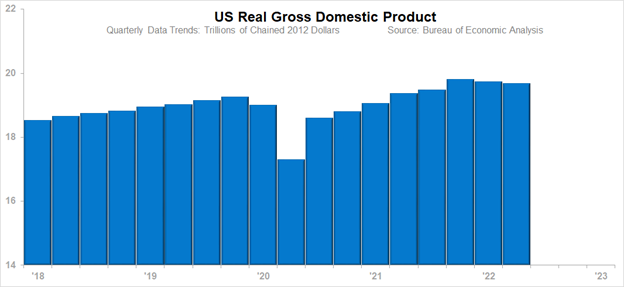

It is official. GDP met the definition of a recession when it declined for a second consecutive quarter based on the 2Q22 advanced release.

It is official. GDP (adjusted for inflation) met the definition of a recession when it declined for a second consecutive quarter based on the 2Q22 advanced release. What this means is now the question.

Clearly companies or markets that benefited from the stimulus money and the circumstances of the pandemic (no travel and people staying at home) are exposed to the weakness suggested by the advanced GDP result. Excess inventory will have to be cleared until such time as the market is back in balance between demand and supply. Expect prices (at all levels in these segments) to be lowered as a means of clearing the excess inventory. For those segments that benefited the most from the COVID-related spending, the return to a balance between supply and demand will be a function of how high demand was above the longer-term trend.

Other parts of the economy will perceive the probable two quarters of decline as a “technical” recession because the pressures that pushed the overall economy downward did not appreciably impact them. These companies are more likely able to benefit from several factors:

It will be a while before the first half of 2022 is officially declared a recession or not. Either way that decision goes, GDP declined during a period we were expecting the economy to be essentially flat. Going into 2022, we had three ways to view the coming year:

We chose view #2 as our guiding principle. Some segments of the economy would go down, more would go up, and on balance we would have an essentially flat trend in GDP. Given the extremely mild first-quarter decline and the even milder second-quarter estimate, that isn’t exactly how it worked out. The economy sagged slightly, while we forecasted an essentially flat trend. We think we missed on the following:

What the missed forecast means:

We don’t think the two quarters of decline in GDP should change your plans for the rest of this year or 2023 in terms of direction and general amplitude. If you receive an EVP service or other specific forecast service from ITR Economics, don’t expect to see many changes, because industry-specific forecasts are not that reliant on GDP for guidance.

If you tie more closely to US Industrial Production than GDP, you have a clearer view into the future. Industrial Production is growing. It is not in recession. Slower growth remains the outlook based on the latest available data from the leading indicators.

The April 2020 to April 2019 year-over-year comparison (1/12 rate-of-change) posted the steepest decline on record.

We receive many questions centered around the 2030s Great Depression. ITR Economics CEO Brian Beaulieu is here to answer 3 of the most common...

ITR Economics CEO and Chief Economist Brian Beaulieu answers three questions we received during the 2030s Great Depression Update webinar on July 27,...