Executive Strategy

Navigating Through Signs of a Recession

See how ITR Economics can help you navigate through signs of a recession to set your company up for a soft landing in the business cycle.

New data shows widespread decline across the manufacturing sector. If the Fed is looking for reasons to lower interest rates, this may be another one.

With the latest data release from the Federal Reserve Board, 2024 is shaping up according to ITR Economics’ expectations, and if you have been following along with us, you know those expectations are not high.

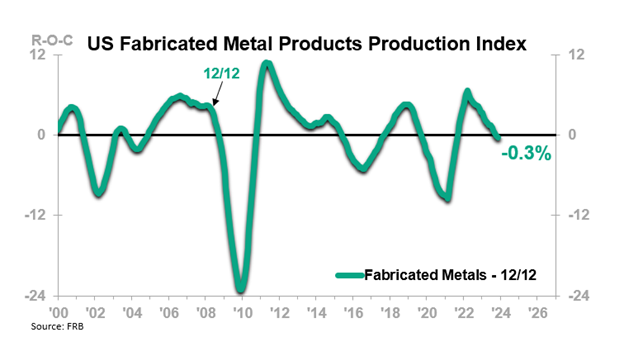

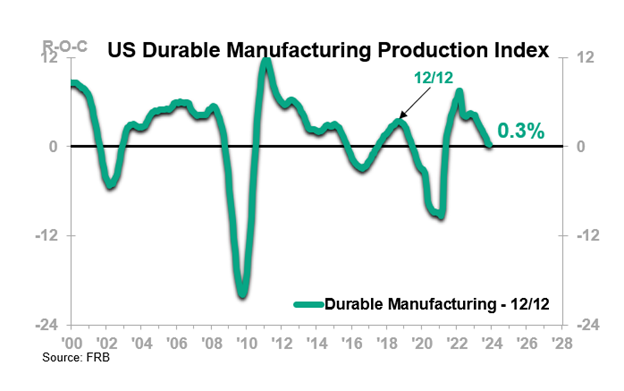

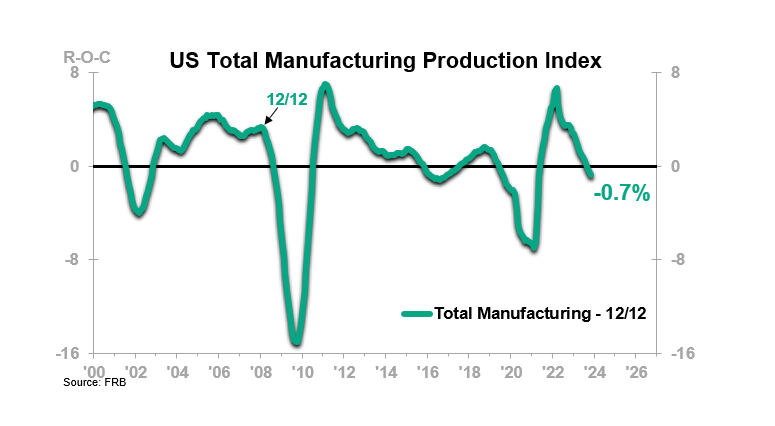

As of the latest Federal Reserve Board data:

This market is only the latest domino to fall.

Other subsegments of Durable Goods Manufacturing currently in Phase D include:

By volume of activity, these segments plus Fabricated Metal Products comprise about half of Durable Goods Manufacturing, meaning that about half of that subsector is in Phase D, Recession.

Meanwhile, the overall Nondurable Goods Manufacturing sector is in Phase D, and overall US Total Manufacturing Production, which includes both the Durable and Nondurable subsectors, is in Phase D. The Federal Reserve Board stated at its last meeting that it was still expecting a soft landing for the US economy, but these manufacturing datapoints – pulled from the Fed’s own data – are indicative of a hard landing per ITR Economics’ methodology.

Readers with business exposure to these Phase D markets should be closely watching their margins and cash position but should also lead with optimism. That does not mean denial regarding the industrial sector recession that is upon us, but rather a resolve borne of both the determination to succeed and the data-driven knowledge that the remainder of the 2020s after this downturn will offer growth-conducive conditions for those well-prepared to leverage them.

It is important to note that the aforementioned datasets are compiled and tracked by the Federal Reserve Board.

Tune into our weekly Fed Watch video series for more insights, but the deteriorating Manufacturing data outlined above is one more factor that could convince the Fed to begin lowering the federal funds rate early this year. If interest rates come down, it would likely result in the yield curve normalizing and ultimately establish a financial backdrop that will allow the mild recession to conclude around year-end.

See how ITR Economics can help you navigate through signs of a recession to set your company up for a soft landing in the business cycle.

Whether your business is facing a soft landing or hard landing, find out how ITR Economics can help steer your company in the right direction!

The economy is exiting a business cycle soft landing. Are we in a recession, or are we not? See what signals the macroeconomy is providing in our...