Keeping up With Commodity Prices

After general decline in industrial commodity prices during 2019, resurgent global growth is poised to spur prices higher this year.

Steel Prices, as measured by the Steel Scrap Producer Price Index , are expected to edge lower as demand wanes in the coming year.

Steel Prices, as measured by the Steel Scrap Producer Price Index, are expected to edge lower as demand wanes in the coming year. Producers are expected to trim prices as they seek to keep production – and profits – rolling.

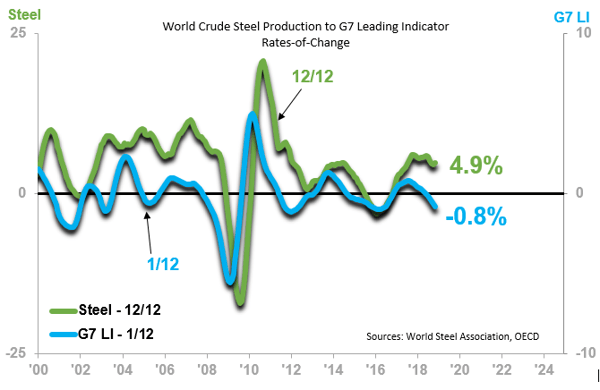

The relationship between global steel production and the G7 Leading Indicator 1/12 is shown on the following chart:

The decline in the G7 Leading Indicator (blue line) is signaling that the decline in the World Industrial Production 12/12 will extend well into 2019. The US, China, and other steel-producing nations will see their industrial production growth trends similarly muted, and in some cases actual decline will occur in the 12MMA trends. The worldwide industrial demand for steel will ease, and prices are expected to ease along with the demand.

Nonresidential Construction, another large market for steel, is expected to improve in many countries, including the US, in 2019. Nonresidential Construction lags industrial production, and thus often appears counter-cyclical. The nascent rate-of-change ascents in the various segments of Nonresidential Construction are expected to extend until late 2019, and that means an increased demand for steel in this segment of the economy. This demand will keep steel prices from cratering, but it is not expected to be strong enough to keep prices from generally moving lower this year. Readers should be wary of inventory buildups at today’s higher prices.

Alan Beaulieu

President

After general decline in industrial commodity prices during 2019, resurgent global growth is poised to spur prices higher this year.

1Q24 US Steel Scrap Producer Prices were 4.1% lower than what they were in 1Q23. What will happen with Steel Prices this year, and what will be the...

Prices are down 25.5% year over year. However, positive developments that occurred throughout the last quarter suggest better days ahead.