Solutions

US Manufacturing – What to Expect in 2022

Read Jackie Greene's most recent blog on manufacturing market trends for 2022. For more information, sign up for our webinar on October 28!

There is a human tendency to believe that we are living through novel times and that the old rules no longer apply. Very rarely is this true.

“It’s different this time.”

We’ve all heard that before. There is a human tendency to believe that we are living through novel times and that the old rules no longer apply. Very rarely is this true. But, with that disclaimer out of the way, I would posit that this time really is different.

The Great Recession of 2008, as with most major business cycles, was triggered by underlying economic factors. The recession of 2020, in contrast, can be quantified as a natural disaster rather than the result of a regular, fundamentals-driven business cycle. The current economic contraction was triggered by a global pandemic, not by economic imbalances that demanded a correction. Recent economic data corroborates the fact that this case really is different.

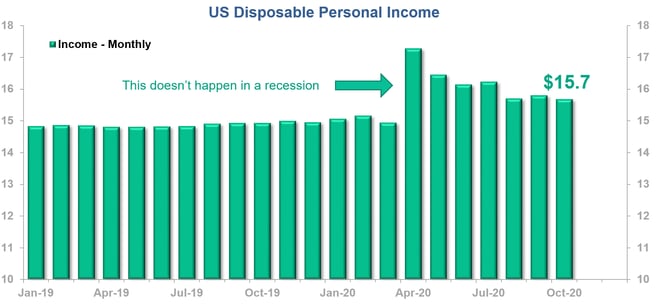

Consumer finances have not exhibited the same negative trends this cycle as in past recessions. Thanks in part to government stimulus efforts, Disposable Personal Income (DPI) has been elevated since the onset of the pandemic. Programs such as the one-time $1,200 stimulus payments and the additional $600 per week in unemployment payments lifted DPI throughout the summer months. Yet DPI through October, after the expiration of those programs, remains above the pre-pandemic level. Also of note, consumers did not spend much of this additional income, as lockdown measures largely prevented travel and in-person shopping and dining. As a result, savings are also elevated, resulting in a historically high level of dry powder available to feed pent-up demand and fuel the recovery.

Trillions of chained 2012 dollars, SAAR. Source: BEA

Employment trends further illustrate the irregular nature of this recession. Although the US Unemployment Rate reached a record 14.4% in April, it has since declined, falling to just 6.4% in November. The Unemployment Rate is declining significantly faster than in most historical recessions as unemployed workers are reabsorbed into the labor force at an abnormally accelerated pace.

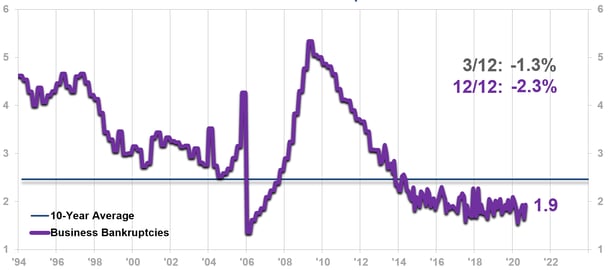

The business response to the 2020 recession also diverges from historical examples. To date, the level of business bankruptcies has not materially increased and remains well below the 10-year average.

Measured in thousands of bankruptcy filings. Source: American Bankruptcy Institute

Yet even more important are the lasting changes to business practices wrought by the pandemic. Throughout this experience, businesses have evolved and adapted in unusual ways. Certain preexisting trends – such as the adoption of work-from-home policies and the growing acceptance of virtual, rather than in-person, meetings – have accelerated. Such changes have tended to come with greater efficiency, cost savings, or both. For example, the “new normal” of virtual meetings may not only result in saved travel costs, but also enable an employee to meet with multiple customers in a day, when in the past that employee may have needed multiple days of travel for a single customer meeting. Many of these new practices will not (and should not) go away following the widespread distribution of a vaccine, and they would not be the natural outcome of a recession borne of a normal, fundamentals-driven business cycle. Those recessions usually only result in changes to corporate governance requirements or banking regulations.

Overall, the recession of 2020 was not a typical recession, and the recovery will not mirror historical precedents either. For businesses, a great starting point would be to consider the last major business cycle and the lessons learned. What do you wish you had done during the onset of the recovery in 2009? But go further. Consider those lessons through the unique lens of 2020. As always, if we at ITR can help focus this discussion, please reach out!

Lauren Saidel-Baker

Economist

Read Jackie Greene's most recent blog on manufacturing market trends for 2022. For more information, sign up for our webinar on October 28!

Here is what we are seeing on the inflation front.

There are so many data points floating by, and cross currents swirling every day that it can be difficult to separate the noise from the worthy.